Japan faces an era-defining reset with the US

After warm relations during his first term, Tokyo has not adapted to Donald Trump’s transactional approach in trade and defence

After warm relations during his first term, Tokyo has not adapted to Donald Trump’s transactional approach in trade and defence

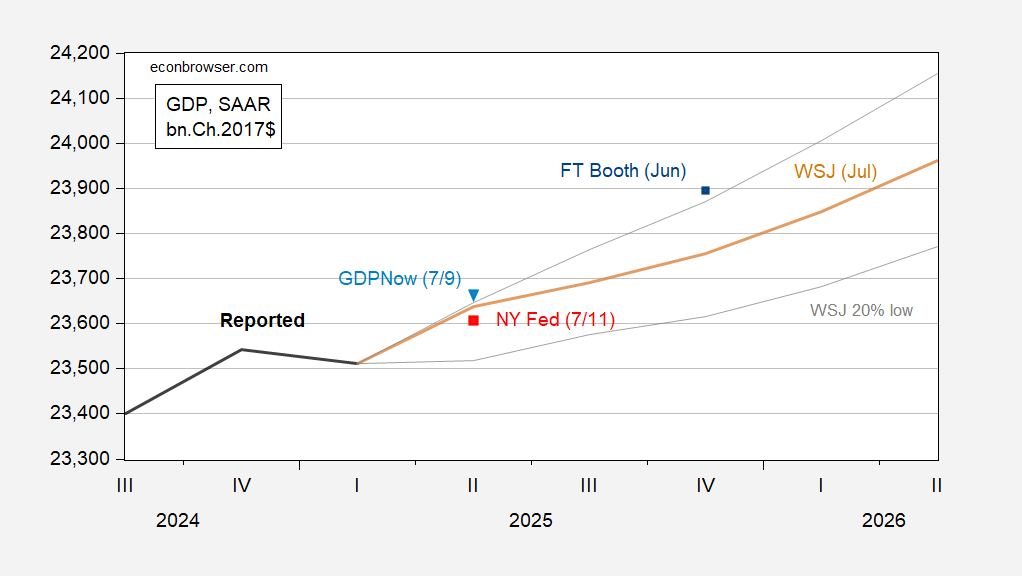

From WSJ July survey out today: Figure 1: GDP (bold black), WSJ July survey mean (tan), lowest/highest 10% based on 2025 q4/q4 growth (gray lines), GDPNow of 7/9 (inverted light blue triangle), NY Fed nowcast of 7/11 (red square), all in bn.Ch.2017$, SAAR. Source: BEA, WSJ, Atlanta Fed, NY Fed, and author’s calculations. Only one forecast is for two consecutive negative quarters of GDP growth (AC Cutts, five consecutive quarters), while there are many forecasts of an individual quarter of negative growth. The WSJ survey mean trajectory is close to the May SPF median. Not surprisingly, the WSJ growth rate for Q2 is just between the Atlanta and NY Fed nowcasts (see here). A cautionary note from the WSJ: Diane Swonk, chief economist at KPMG US, cautioned that official economic indicators, which combine actual data from surveys with estimates, often struggle to capture inflection points. “As good as our stats are, they just weren’t made for these kinds of very large moves in policy that cause a knee-jerk reaction,” Swonk said. “It makes it even harder to read the tea leaves.” Trump’s policies—which besides tariffs include a clampdown on illegal immigration, stepped-up deportations and a just-signed megabill cutting taxes and some spending—may also take time to filter into the real economy.

UK chancellor delivers Mansion House speech, Fed issues Beige Book and China releases second-quarter GDP data

European Commission president Ursula von der Leyen calls for negotiated solution to dispute

Market Questions is the FT’s guide to the week ahead

Businesses wonder if Hanoi locked in better terms on tariffs by moving quickly — or gave up too much

Companies await details on whether 50% levy will apply to all products containing the metal

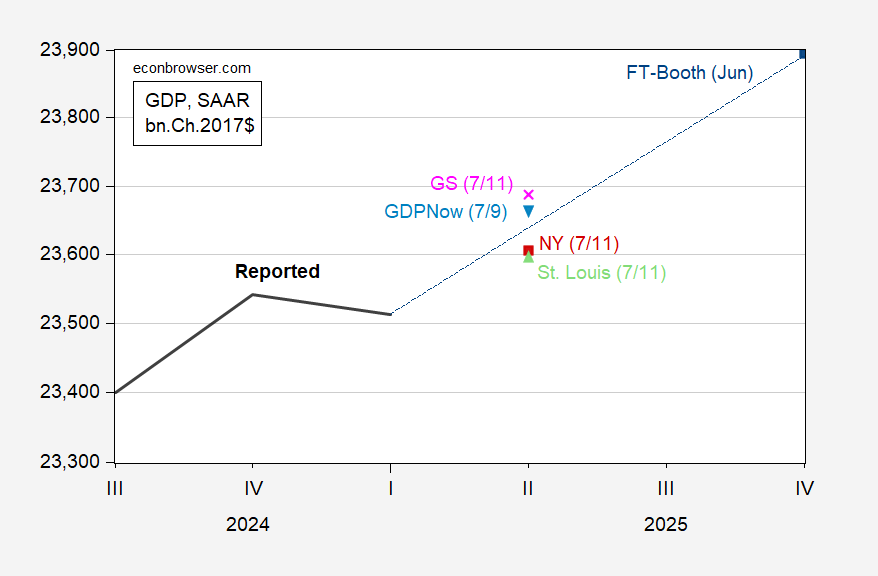

As of today: Figure 1: GDP (bold black), GDPNow of 7/9 (light blue inverted triangle), NY Fed nowcast of 7/11 (red square), St. Louis Fed news nowcast of 7/11 (light green triangle), Goldman Sachs of 7/11 (pink x), FT Booth June survey median (blue square), all in bn.Ch.2017$ SAAR. Source: BEA, Atlanta, NY, St. Louis Feds, Goldman Sachs, FT-Booth, and author’s calculations. The Atlanta Fed nowcast (GDPNow) is a bottom up (component by component forecast), while the NY Fed nowcast is top down. The St. Louis index uses data surprises to generate the nowcast of aggregate GDP growth. Given the nature of the distortions attendant tariff front-loading, I would put more weight on the Atlanta Fed nowcast (it predicted negative growth, while the NY Fed and St. Louis Fed nowcasts predicted positive). Final sales to private domestic purchasers (aka “core GDP”) should be less sensitive to distortions. Figure 2: Final sales to private domestic purchasers (bold black), GDPNow of 7/9 (light blue inverted triangle), in bn.Ch.2017$ SAAR. Source: BEA, Atlanta Fed, and author’s calculations. The Atlanta Fed nowcasts a slight decline (0.9% annualized) in final sales to private domestic purchasers. As is, reported sales are far below the median forecast of the May Survey of Professional Forecasters.

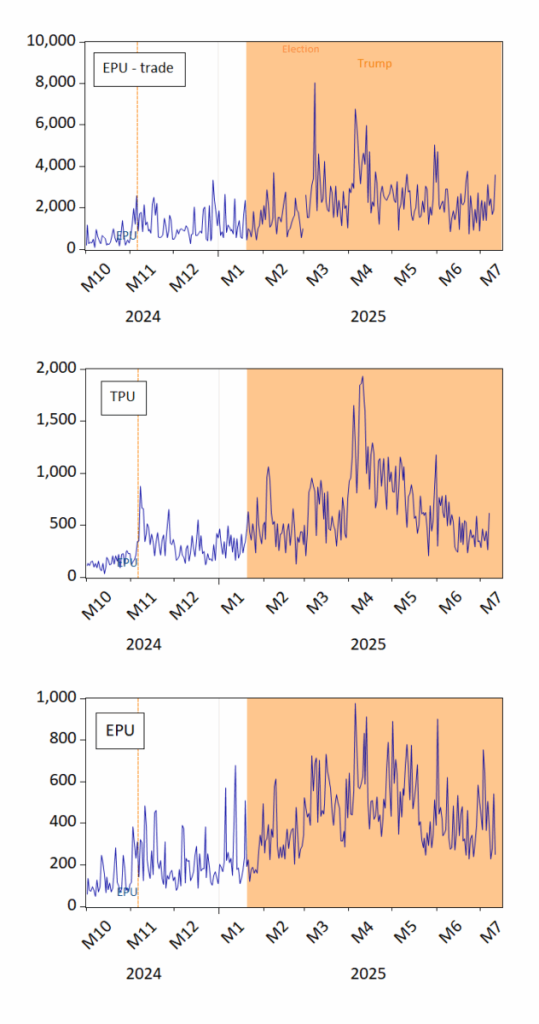

See here and here. Every morning I wake up, think I can’t see anything more crazy than what occurred yesterday, and then I check the news. Figure 1: Top panel, EPU-trade; Middle panel: Trade Policy Uncertainty; Bottom panel: EPU. Orange shading denotes second Trump administration. Orange dashed line denotes election. Source: policyuncertainty.com, Iacoviello et al.

US president issues new threats against trading partners in letters posted to social media