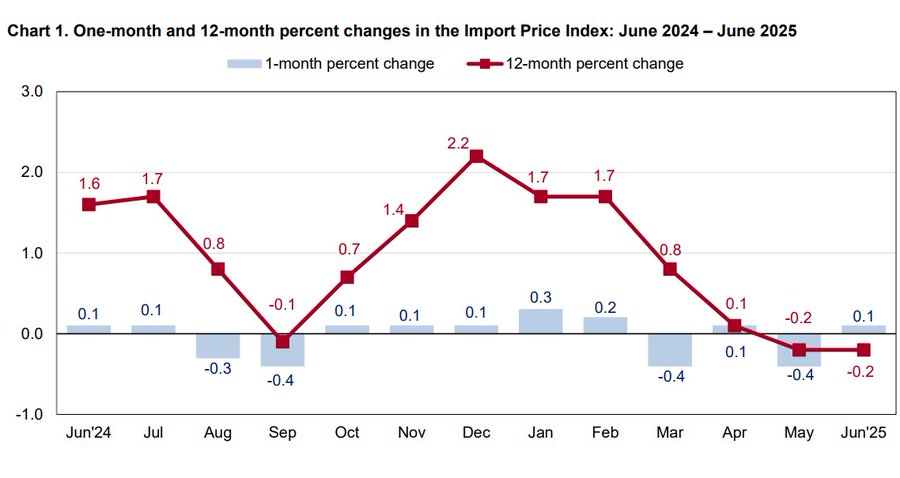

EJ Antoni on the No Tariff Pass Through Thesis

From Heritage Chief Economist EJ Antoni on X: N.B.: this is an INDIRECT indicator of tariffs not being passed on b/c import prices have fallen relative to their domestic counterparts; that’s the result of a substitution effect and foreign producers’ attempt to retain market share by reducing their prices relatively speaking: · Jul 17 Import prices just came in WAAAY below expectations: June was up just 0.1% M/M, -0.2% Y/Y, while May saw a huge downward revision from flat to -0.4% M/M; still waiting for tariffs to be passed on by foreign producers… Note that Dr. Antoni is apparently using the all commodity imports price index. I think that, since no tariffs have been applied to oil, it would be more appropriate to use the import price index ex-petroleum. Using this index, and Instead of plotting rates of change, I show price indices relative to 2025M04, given that the 10% tariffs were effective in early April. Figure 1: Import price index for all commodities (blue), for commodities ex-petroleum (tan), all in logs 2025M04=0. Source: BLS via FRED, and author’s calculations. Using this more appropriate series, I do not see the price decrease the Dr. Antoni refers to. As an aside, I am still waiting for Dr. Antoni to declare the end of the recession he claimed started in 2022.