EU pauses trade retaliation against US after Trump’s 30% tariff threat

European Commission president Ursula von der Leyen calls for negotiated solution to dispute

European Commission president Ursula von der Leyen calls for negotiated solution to dispute

Market Questions is the FT’s guide to the week ahead

Businesses wonder if Hanoi locked in better terms on tariffs by moving quickly — or gave up too much

Companies await details on whether 50% levy will apply to all products containing the metal

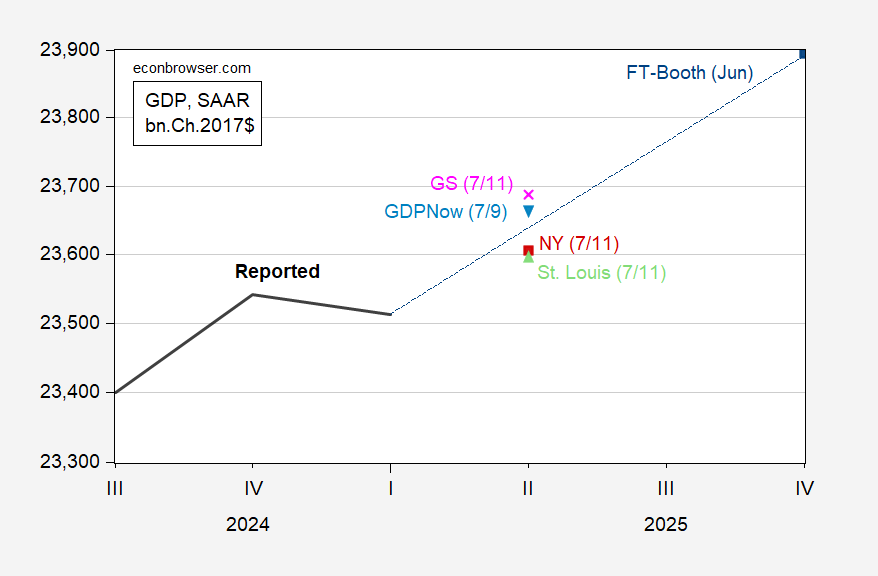

As of today: Figure 1: GDP (bold black), GDPNow of 7/9 (light blue inverted triangle), NY Fed nowcast of 7/11 (red square), St. Louis Fed news nowcast of 7/11 (light green triangle), Goldman Sachs of 7/11 (pink x), FT Booth June survey median (blue square), all in bn.Ch.2017$ SAAR. Source: BEA, Atlanta, NY, St. Louis Feds, Goldman Sachs, FT-Booth, and author’s calculations. The Atlanta Fed nowcast (GDPNow) is a bottom up (component by component forecast), while the NY Fed nowcast is top down. The St. Louis index uses data surprises to generate the nowcast of aggregate GDP growth. Given the nature of the distortions attendant tariff front-loading, I would put more weight on the Atlanta Fed nowcast (it predicted negative growth, while the NY Fed and St. Louis Fed nowcasts predicted positive). Final sales to private domestic purchasers (aka “core GDP”) should be less sensitive to distortions. Figure 2: Final sales to private domestic purchasers (bold black), GDPNow of 7/9 (light blue inverted triangle), in bn.Ch.2017$ SAAR. Source: BEA, Atlanta Fed, and author’s calculations. The Atlanta Fed nowcasts a slight decline (0.9% annualized) in final sales to private domestic purchasers. As is, reported sales are far below the median forecast of the May Survey of Professional Forecasters.

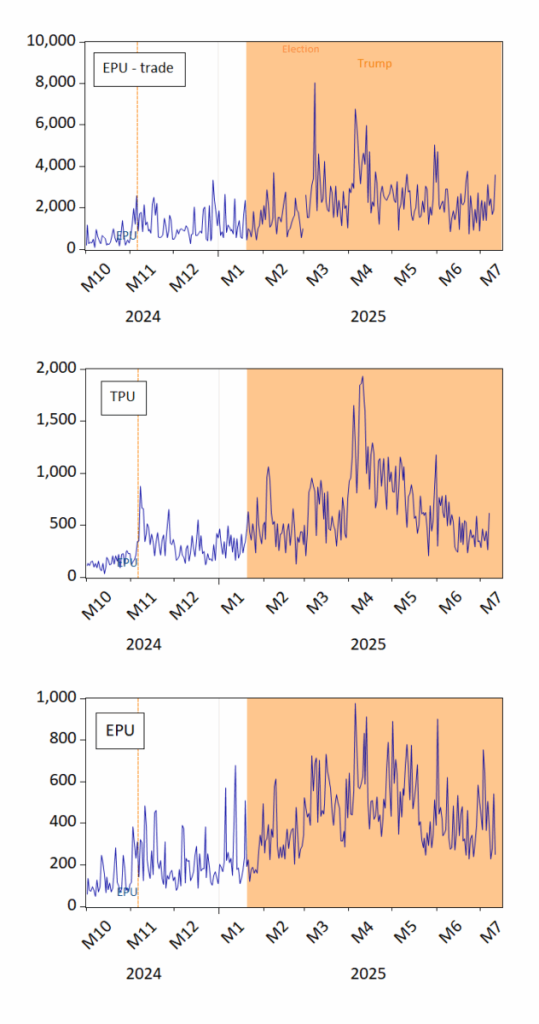

See here and here. Every morning I wake up, think I can’t see anything more crazy than what occurred yesterday, and then I check the news. Figure 1: Top panel, EPU-trade; Middle panel: Trade Policy Uncertainty; Bottom panel: EPU. Orange shading denotes second Trump administration. Orange dashed line denotes election. Source: policyuncertainty.com, Iacoviello et al.

US president issues new threats against trading partners in letters posted to social media

Lesotho, which supplies Levi’s and Wrangler, declares ‘state of disaster’ as Trump threat triggers job cuts

Fund managers and bankers cast doubt on bets US president will back down from most severe threats

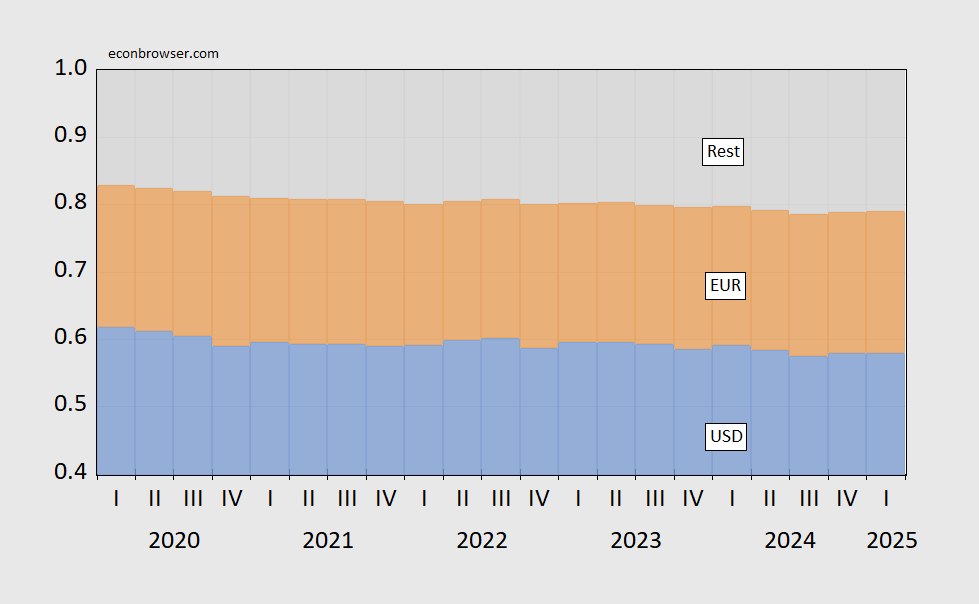

Based on IMF data (COFER, IFS): Figure 1: USD shares of fx (blue bars), EUR (tan), all other (gray). USD(EUR) share assumes 60%(35%) of unallocated reserves are in USD(EUR). Source: IMF COFER, and author’s calculations. The drop in USD reserves out of total FX reserves is not apparent. However, gold has taken on a heightened importance in recent years. Taking this into account, we have Figure 2. Figure 2: USD shares of fx and gold reserves (blue bars), EUR (tan), all other (gray), and gold (yellow). USD(EUR) share assumes 60%(35%) of unallocated reserves are in USD(EUR). Assumes quantity of gold holdings stay constant in 2025Q, and observed . Source: IMF COFER, World Gold Council, and author’s calculations. To the extent that total reserves are the relevant measure, the dollar has dropped by 1.4 percentage points in 2025Q1; the standard deviation of changes is 0.6 ppts. If central banks on net acquired gold in Q1 (World Gold Council suggests 50 tonnes whereas I assumed 0 tonnes), then the drop would be even larger.