Political pressure on the Fed: an historical echo from Canada

When firing backfires

Agreement would mirror accord with Japan and head off Trump’s threat to raise duties to 30%

Yields for investment-grade EM borrowers fall relative to developed markets amid concerns over traditional havens

Also in today’s newsletter, McKinsey bars China AI work and UniCredit pulls BPM offer

Chancellor Friedrich Merz’s government wants to threaten a strong response if US is not prepared to compromise

There are lessons for central banks from past episodes of high inflation combined with weak growth

Also in this newsletter: Why Brussels and Beijing want to keep a united front against the US despite differences

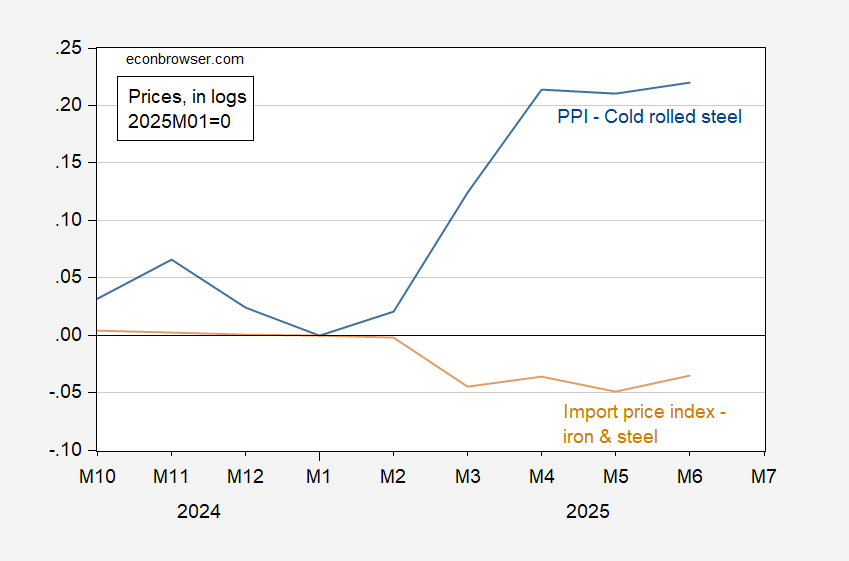

Recall CEA has asserted that imported goods prices (incl tariffs) have fallen relative to domestically produced, based on conjoining 2017 IO tables and PCE data. I wondered whether imported goods prices and prices of close substitutes have fallen. To investigate, I do something simpler: look at steel import prices (ex-tariffs) and steel PPI (incl. tariffs). Figure 1: Import price index for iron and steel (tan), PPI for cold rolled steel (blue), both in logs 2025M01=0. Source: BLS, and author’s calculations. Effective June 4, a 50% Section 232 tariff has been in effect, rising from the previous 25%. Since January 2025, the import price index has fallen 3.5%, while the steel/iron PPI has risen 22% (log terms). So as the 50% tariff comes into play, we should expect — on net — continued increases in the price of steel. More discussion at NYT.