EU gears up for tough China talks in shadow of trade tensions and Ukraine war

Ursula von der Leyen and António Costa prepare to meet Xi Jinping in Beijing amid geopolitical turmoil

Ursula von der Leyen and António Costa prepare to meet Xi Jinping in Beijing amid geopolitical turmoil

Japanese Prime Minister Shigeru Ishiba says he will ‘examine the details’ as US president announces 15% tariff

Cut in guidance by Finnish telecoms equipment maker highlights how European groups are being hurt by US policy

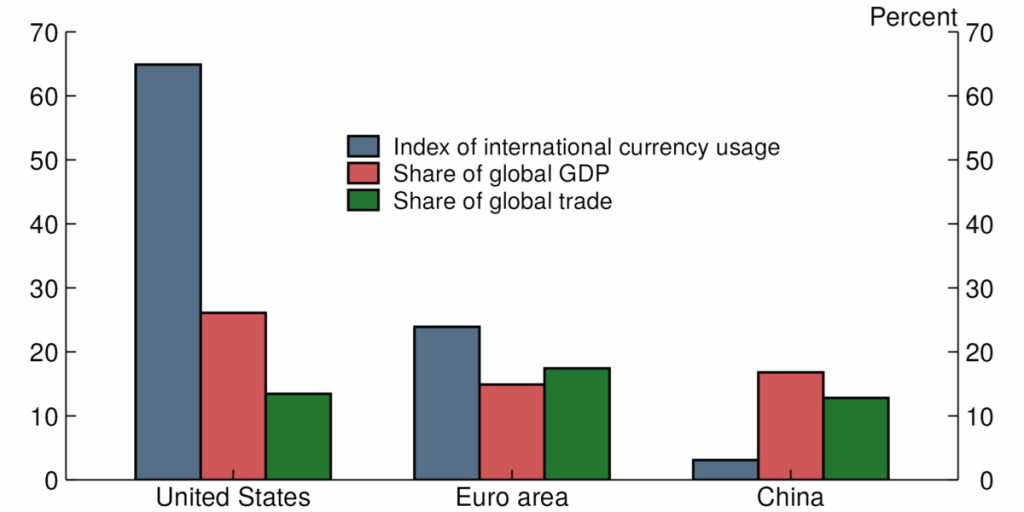

FEDS note published on Friday: The role of the U.S. dollar has received renewed attention this year. A sharp rise in policy uncertainty has led some to question the strength and stability of the U.S. economy. In particular, increased attention has been paid to the U.S. fiscal outlook, as noted in the recent downgrade by Moody’s of the credit rating on U.S. government debt. And the U.S. has increased its level of tariffs and thereby somewhat reduced its openness to trade flows. Given that most data on international dollar usage is available with a lag, this note is not yet able to show any potential results of the change in the U.S. credit rating or changes to tariff rates in 2025. Rather, it provides a baseline for where the international role of the dollar stood before these announcements. In particular, we can examine the longer-run effects of U.S. sanctions on Russia that were imposed following its invasion of Ukraine in 2022. From the Note: Source: Bertaut et al. (2025).Sc I think there is a bit of understatement with respect to the potential impact of recent statements, including (1) “Liberation Day” and aftermath, (2) ongoing assaults on Fed independence by Trump et al. In particular, Steven Kamin’s analysis of time-variation in the VIX-dollar correlation is noted in this recent Economist piece. Torsten Slok in today’s examination identify what correlates are necessary to explain the recent dollar-interest rate divergence (hint: includes tariffs but also a post-“Liberation Day” dummy, trade policy uncertainty measure, and cumulative mentions of “Mar-o-Lago accord”. Personally, I like looking at the USD-10yr TIPS correlation over three “crisis” episodes: Figure 1: Scatterplot of USD value against 10 year TIPS, around Lehman (blue), around Covid-19 (red), and around “Liberation Day” (green). Source: Federal Reserve Board and Treasury via FRED. Currently working on a paper with Jeffrey Frankel and Hiro Ito, on assessing central bank holdings of reserves, including gold, and how those holdings have changed with the use of sanctions and in the presence of geopolitical factors. More on that soon.

Brussels needs to be ready to unleash its anti-coercion armoury

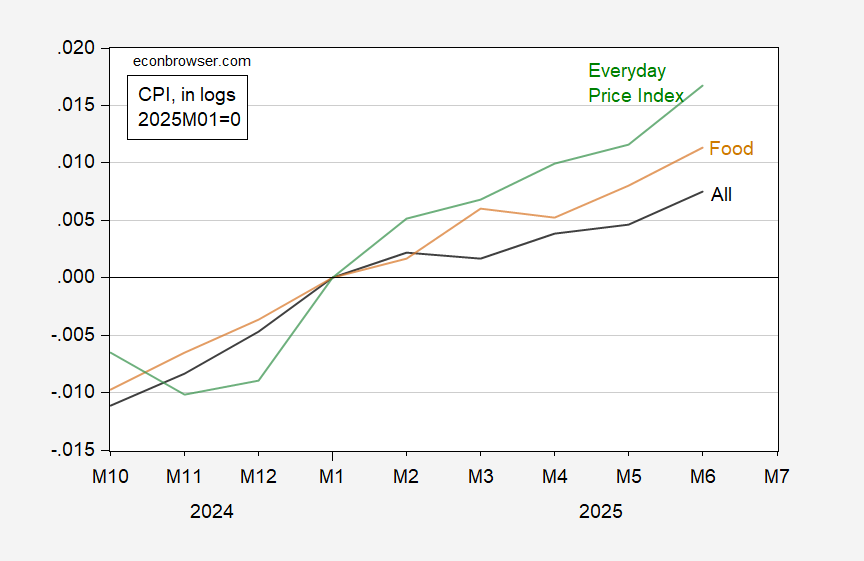

How’s dropping prices for everyday folks going? Figure 1: CPI all (black), CPI for food (tan), Everyday Price Index (green), all in logs, 2025M01=0. Source: BLS, AIER, and author’s calculations. Median household income CPI is not available for 2025. However, over 2024, it tracks the CPI overall (both in nsa terms) very closely. Hence, extrapolating forward, the CPI all should proxy fairly well median income CPI. As noted in the last post, data collection has declined over the past few years, due to budget constraints. One might hope to access alternative measures would shed light on whether the reported CPI has experienced degradation in accuracy. However, in some instances, alternatives are merely transformations of BLS reported data. For instance, the AIER’s Everyday Price Index (“EPI”) is a weighted average of a subset of CPI categories.

The Commerce Department eliminated two advisory committees on economic statistics gathering (see Marketplace). BLS received some additional funds in March as part of a continuing resolution; however the Trump budget proposal includes an 8% reduction in budget in nominal terms. The BLS, tasked with compiling the CPI as well as other labor market indicators (employment, wages) has been already stretched by stagnant funding colliding with escalating costs. Recently, this has affected compilation of the CPI. More and more prices are imputed. Source: Economist. Of course, none of this should come as a surprise. A lot of this was prefigured in the Project 2025 (as I documented here). There’s hardly any money to be saved by slashing in real terms funding for the statistical agencies, so one has to wonder what the underlying philosophy of the Trump administration is. Perhaps, it’s the philosophy of “if a recession occurs, and it’s not measured, will anybody notice?” Perhaps, given Trump’s assault on the Fed’s independence, my guess is that it’s more likely “if inflation accelerates and inflation is not measured, will anybody notice?”. In any event, June’s FT-Booth survey of macroeconomists was interesting insofar as no one thought that the Administration’s measures would improve data quality. Source: FT-Booth June Survey of Macroeconomists. I was in the “very worried” category. Apparently, one macroeconomist would not be worried. I think he/she is in denial.

First statistical rejig in more than a decade makes debt ratios appear healthier

Sector faces threat of levies as high as 200% on overseas imports

The One Big Beautiful Bill Act loosens fiscal policy; the Fed will need to decide whether to tighten in response