Franco-German engine hums as Merz and Macron meet in Berlin

Also in this newsletter: Why Brussels and Beijing want to keep a united front against the US despite differences

Also in this newsletter: Why Brussels and Beijing want to keep a united front against the US despite differences

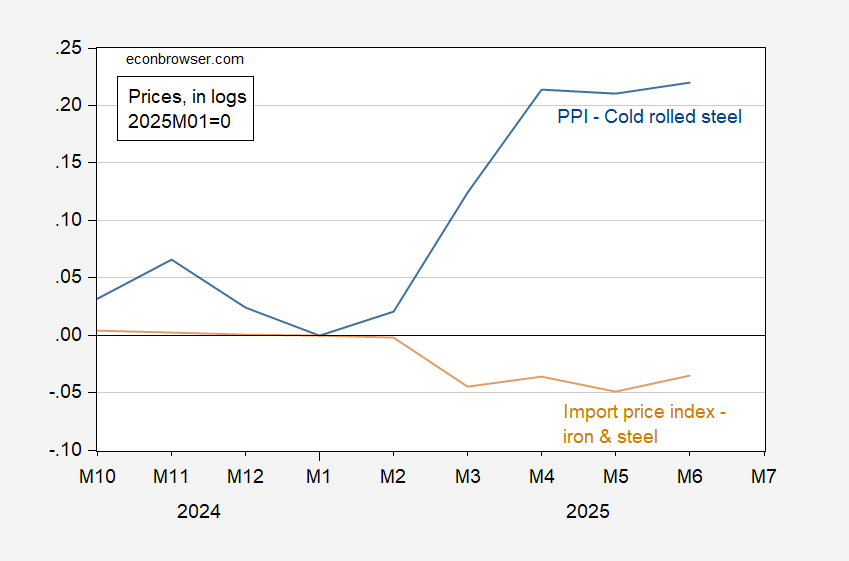

Recall CEA has asserted that imported goods prices (incl tariffs) have fallen relative to domestically produced, based on conjoining 2017 IO tables and PCE data. I wondered whether imported goods prices and prices of close substitutes have fallen. To investigate, I do something simpler: look at steel import prices (ex-tariffs) and steel PPI (incl. tariffs). Figure 1: Import price index for iron and steel (tan), PPI for cold rolled steel (blue), both in logs 2025M01=0. Source: BLS, and author’s calculations. Effective June 4, a 50% Section 232 tariff has been in effect, rising from the previous 25%. Since January 2025, the import price index has fallen 3.5%, while the steel/iron PPI has risen 22% (log terms). So as the 50% tariff comes into play, we should expect — on net — continued increases in the price of steel. More discussion at NYT.

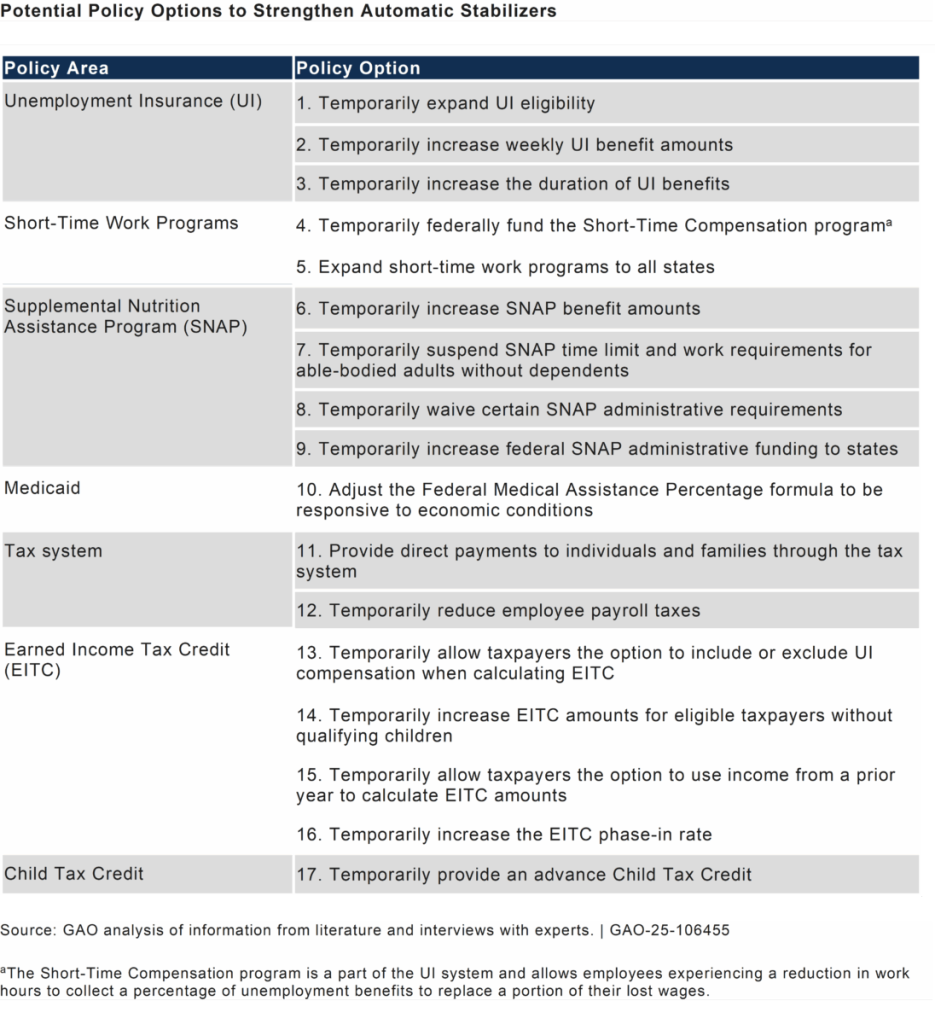

I think we’ll need these sooner than you think. But legislation has just been passed to disable these supports. From GAO, “During Past Recessions and Economic Downturns, These Factors Supported an Effective Fiscal Response,” July 15, 2025. GAO identified four principles that could be used to assess the design or reform of automatic stabilizers. Information from literature and economic and social policy experts suggests that effective automatic stabilizers are timely, temporary, targeted, and predictable. Within those four broad principles, GAO identified eight factors that contribute to the effective design of automatic stabilizers (see table). To my knowledge, recent legislation goes the other direction, at least insofar as Medicaid and SNAP are concerned. Entire report here.

Jakarta and Washington release deal framework while US president says Philippines will pay 19% rate

Ursula von der Leyen and António Costa prepare to meet Xi Jinping in Beijing amid geopolitical turmoil

Japanese Prime Minister Shigeru Ishiba says he will ‘examine the details’ as US president announces 15% tariff

Cut in guidance by Finnish telecoms equipment maker highlights how European groups are being hurt by US policy

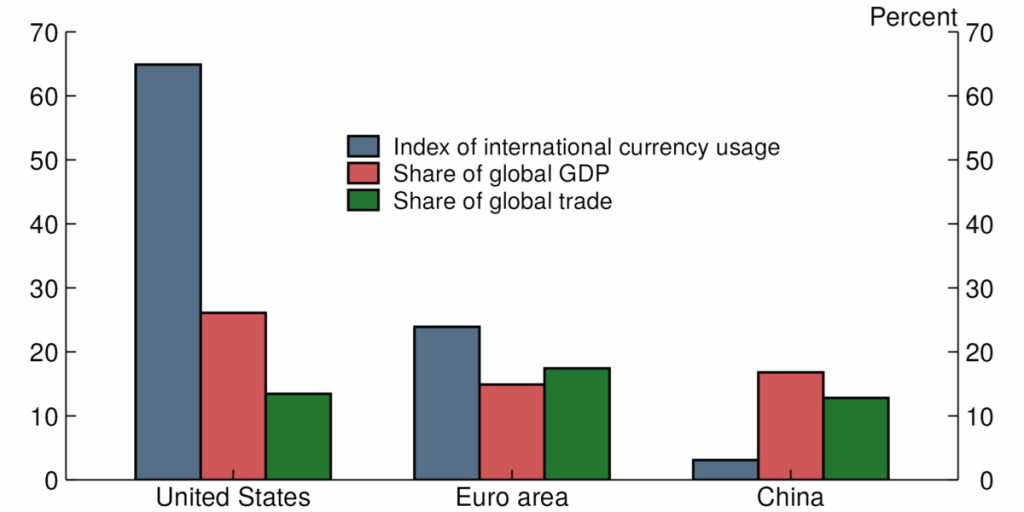

FEDS note published on Friday: The role of the U.S. dollar has received renewed attention this year. A sharp rise in policy uncertainty has led some to question the strength and stability of the U.S. economy. In particular, increased attention has been paid to the U.S. fiscal outlook, as noted in the recent downgrade by Moody’s of the credit rating on U.S. government debt. And the U.S. has increased its level of tariffs and thereby somewhat reduced its openness to trade flows. Given that most data on international dollar usage is available with a lag, this note is not yet able to show any potential results of the change in the U.S. credit rating or changes to tariff rates in 2025. Rather, it provides a baseline for where the international role of the dollar stood before these announcements. In particular, we can examine the longer-run effects of U.S. sanctions on Russia that were imposed following its invasion of Ukraine in 2022. From the Note: Source: Bertaut et al. (2025).Sc I think there is a bit of understatement with respect to the potential impact of recent statements, including (1) “Liberation Day” and aftermath, (2) ongoing assaults on Fed independence by Trump et al. In particular, Steven Kamin’s analysis of time-variation in the VIX-dollar correlation is noted in this recent Economist piece. Torsten Slok in today’s examination identify what correlates are necessary to explain the recent dollar-interest rate divergence (hint: includes tariffs but also a post-“Liberation Day” dummy, trade policy uncertainty measure, and cumulative mentions of “Mar-o-Lago accord”. Personally, I like looking at the USD-10yr TIPS correlation over three “crisis” episodes: Figure 1: Scatterplot of USD value against 10 year TIPS, around Lehman (blue), around Covid-19 (red), and around “Liberation Day” (green). Source: Federal Reserve Board and Treasury via FRED. Currently working on a paper with Jeffrey Frankel and Hiro Ito, on assessing central bank holdings of reserves, including gold, and how those holdings have changed with the use of sanctions and in the presence of geopolitical factors. More on that soon.

Brussels needs to be ready to unleash its anti-coercion armoury